How Much Do I Have to Pay in Health Care

What percent of health insurance is paid by employers?

When you're considering a new health insurance program, your organization's contribution strategy is an important decision. In simple terms, how much will employees pitch in for coverage, and what percentage will be paid by the employer? With traditional group health insurance plans, the organization must contribute a minimum percentage, leaving the employees to pay the remaining amount, usually through a payroll deduction. So just what percent do employers typically pay in the United States? Across the country, a Kaiser Family Foundation survey found that the average percent of health insurance paid by employers is 83% for single coverage and 73% for family coverage. Let's dive into these stats a little deeper. Find out the average cost of health insurance in your area in our state-by-state guide In 2020, the standard company-provided health insurance policy totaled $7,470 a year for single coverage. On average, employers paid 83% of the premium, or $6,200 a year. Employees paid the remaining 17%, or $1,270 a year. For family coverage, the standard insurance policy totaled $21,342 a year with employers contributing, on average, 73%, or $15,579. Employees paid the remaining 27% or $5,763 a year. While large employers contribute a significant amount to employees' healthcare, small employers tell a different side of the story. 27% of covered workers in small firms are in a plan where the employer pays the entire premium for single coverage, compared to only 4% of covered workers in large firms. Similarly, 28% of covered workers are in a plan where they must contribute more than half of the premium for family coverage, compared to 4% of covered workers in large firms. A likely reason for this is that small businesses simply can't afford to make the kind of contributions larger employers can. After all, even a 50% contribution may be more than what's available in a small employer's benefits budget. Considering that only 48% of firms with three to nine workers offer coverage compared to virtually all firms with 1,000 or more workers that offer coverage, small employers may also feel that they don't have enough employees to make investing in health benefits worth it at all. in order to offer a health benefit at all. Not only do small employers have tighter budgets to begin with, the rising cost of health insurance makes it even harder to offer a benefit. The average premium for family coverage has increased 22% over the last five years and 55% over the last ten years, significantly more than either workers' wages or inflation. This steady increase in costs can make it difficult for small employers with tight budgets to continue to offer employees with a health benefit that will provide enough value. As many small employers tend to struggle with meeting minimum health insurance contribution requirements, alternative contribution strategies and arrangements prove to be helpful. For example, instead of paying for a company-provided health insurance policy, many small employers are providing a health reimbursement arrangement (HRA)—an arrangement in which employers give employees an allowance toward their individually-purchased health insurance premiums. Because these arrangements allow employers to personally define their contribution, small organizations often find them to be the more affordable option. The reimbursement process for employers and employees include the following steps: There are two great options for employers who decide they can't afford traditional group health coverage for all of their employees. A qualified small employer HRA (QSEHRA) is a health benefit for employers with fewer than 50 full-time equivalent employees who don't want to offer employees group health insurance. With a QSEHRA, employers reimburse employees tax-free for their medical expenses, including individual health insurance premiums up to a maximum contribution limit. Check out our latest QSEHRA annual report to see how a QSEHRA helped our customers last year. Download our beginner's guide to QSEHRA The individual coverage HRA (ICHRA) is a health benefit for employers of all sizes. With an ICHRA, small organizations can reimburse employees tax-free for individual health insurance premiums and other medical expenses. It can function as a stand-alone benefit or as a separate option in an organization's health benefits program, alongside group health insurance. There are no limits for company size and no restrictions for allowance amounts. Download our beginner's guide to ICHRA When looking at what percent of health insurance is paid by employers, we see that there are differences between small and large employers. While most large employers offer some kind of traditional group health insurance and cover the majority of their employees' premiums, small businesses are less likely to be able to select traditional health insurance due to cost, less market options, size, and low flexibility. Because of this, many small employers are taking a second look at individual health insurance paired with budget-friendly health reimbursement arrangements, such as an ICHRA or QSEHRA, that will allow them to choose an allowance that will work for them and their employees. To find out how an HRA will work for you and your business needs, schedule a call with a personalized benefits advisor at PeopleKeep for help getting started. This article was originally published on August 12, 2020. It was last updated on September 24, 2021. Employers pay 83% of health insurance for single coverage

Small employers contribute significantly less to family coverage

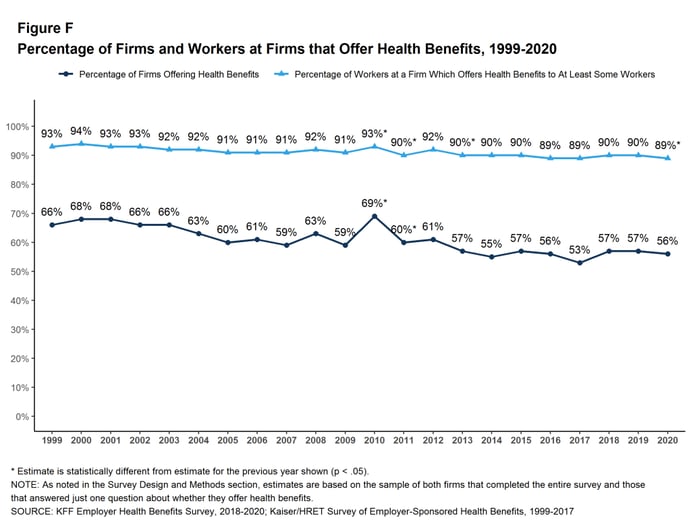

Percentage of firms offering health benefits

Alternative contribution strategies

How HRAs work

Qualified small employer HRA (QSEHRA)

Individual coverage HRA (ICHRA)

Conclusion

Topics: Group Health Insurance, Kaiser Family Foundation, Premiums, Small Group Health Insurance, Qualified Small Employer HRA, Healthcare Costs, Individual Coverage HRA

How Much Do I Have to Pay in Health Care

Source: https://www.peoplekeep.com/blog/what-percent-of-health-insurance-is-paid-by-employers

0 Response to "How Much Do I Have to Pay in Health Care"

Post a Comment